Should I claim social security early or delay and take it later? A question that every retiree / couple has to answer for themselves. Here are the main factors you need to consider when deciding to claim early or delay.

Delay

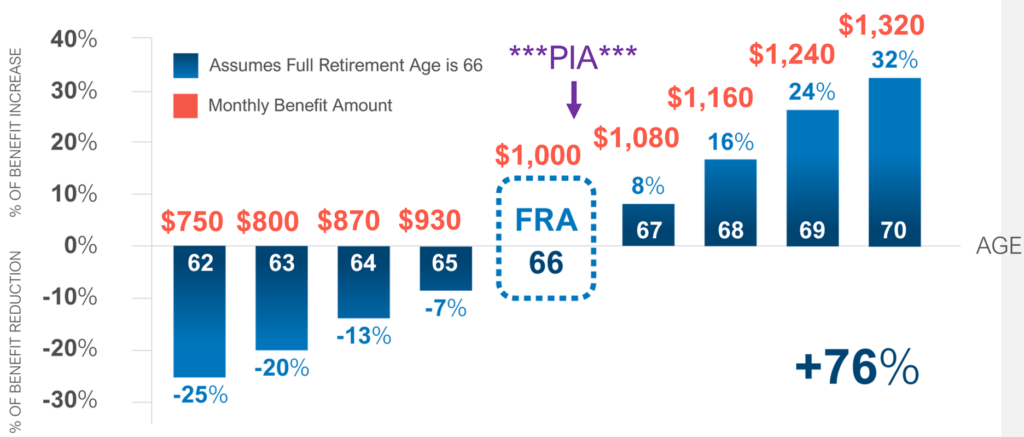

1) ~76% difference in monthly pay

To keep it simple, let’s just assume your Full Retirement Age (“FRA”) is age 66 and you have a Primary Insurance Amount (“PIA”) of $1,000. As you can see in the chart below, if you decide to claim at age 62, you will have reduced benefits of about 25%. If you wait until age 70, you’ll be able to increase your monthly benefit by 32%, not counting Cost of Living Adjustments (“COLA”).

2) Where else can you get a guaranteed 8%?

Referring still to the chart above, the coolest part about this is once you hit your FRA, for every year you delay further, you will get a guaranteed 8% bump on top of inflation for a maximum increase of 32% by age 70 (24% if your FRA is 67). Where else can you get a guaranteed 8% return?! This is on top of inflation. So, for instance, if you had turned your FRA in 2022 and decided to delay benefits a year, you would have received an 8% bump plus an 8.7% Cost of Living Adjustment (“COLA”) for a total increase of 16.7%!

3) We are living longer – protect your spouse

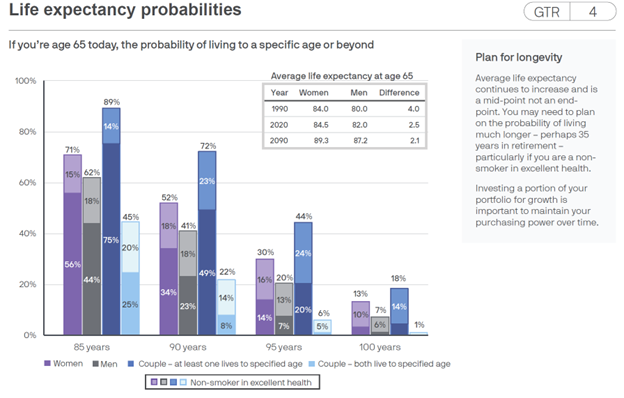

If you are married and there is a significant difference in each spouse’s PIA, this is the single most important reason to delay claiming benefits, at least for the primary earner. We are living longer than ever. As the chart below by JPMorgan shows, once you have made it to 65, assuming there are no serious health challenges, you have a significant chance (72%) of at least one of you making it to age 90.

https://am.jpmorgan.com/us/en/asset-management/adv/insights/retirement-insights/guide-to-retirement/guide-to-retirement-slides/guide-to-retirement-retirement-landscape/gtr-expectancy/

This means you should be planning on making your money last for significantly longer than just the average life expectancy, and social security is a big part of that. What’s more, when the primary earner passes away, the secondary (lesser) earner will lose his or her benefit and take over the benefit of the deceased primary earner. Thus, in cases where the primary earner makes a great deal more than the secondary earner, it is critical that the primary earner maximizes what he or she makes from social security. They can do that by waiting until age 70 to claim. In fact, one common social security strategy is to have the secondary earner file on their own record early or at FRA while the primary earner delays until age 70. Once the primary earner turns on his/her social security, the secondary earner can receive the spousal boost to half of the primary earner’s benefit.

4) Tax Efficiency!!

I know, I know… shocking that a CPA includes a point about taxes in the list, but at least it didn’t make an appearance until #4, right?!

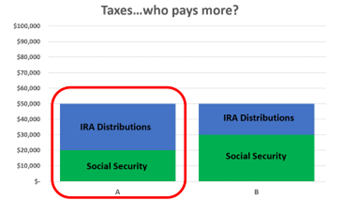

For most retirees, taxes and healthcare are locked in a constant gun battle to be the most expensive line item throughout their retirement. The good news is, if you plan ahead, you can minimize some of those costs. For an in-depth discussion on this topic and various strategies, click here. In short, however, we can utilize social security to minimize our taxes by maximizing the amount of our income that comes from social security. Because social security is tax-favorable, and granted that’s a generous term to describe something that prior to 1983 was tax free, it is better to show income from social security on a tax return than it is to show income from wages or IRA distributions.

For example, assume that Family A and Family B each need 50k in income during retirement. They are equal in every way except that Family A claimed social security earlier than did Family B, so their Social Security benefit is lower. Even though both families need 50k of income per year, Family A will pay more in taxes than Family B, since a greater portion of its income comes from IRA Distributions as opposed to Social Security.

Early

1) I need the money. We can talk all day about strategies in retirement and how to maximize social security. At the end of the day, however, if you need the money, take it! Every strategy we take is designed to increase quality of life in retirement, so if claiming early means your quality of life will go up, please take it! As long as you are educated on your options and are comfortable with what your are giving up, you know best what your financial situation looks like.

2) With my health, I likely won’t live long enough to justify delaying. If you refer back to the ‘Life expectancy probabilities’ chart above, you’ll note that these are broad averages of 65 year olds. If you already know that you have a health condition that will likely prevent you from a living into your 80s and 90s, maybe it does make sense to claim early. However, make sure that you are also considering the longevity of your spouse in your decision.

3) I have a qualifying child. Those who have children under the age of 18 (or who are 18 but still in high school OR have a disability that began before age 22) can claim a child benefit. This is similar to a spousal benefit in that they would receive half of the parent’s Primary Insurance Amount. If this is your situation, it may make sense to claim early so your child can get a benefit off of your benefit before they age out. However, make sure you are also considering the family maximum and the work rules in your decision.

Josh Bretl is a CPA who loves working with retirees. Josh teamed up with his father in 2003 at FSR Certified Public Accountants, Ltd. to build secure financial futures for retirees and pre-retirees in the greater Chicago area. He is proud to work at a family-owned firm that specializes in tax-focused retirement strategies.

Josh Bretl is a CPA who loves working with retirees. Josh teamed up with his father in 2003 at FSR Certified Public Accountants, Ltd. to build secure financial futures for retirees and pre-retirees in the greater Chicago area. He is proud to work at a family-owned firm that specializes in tax-focused retirement strategies.

0 Comments