Maximize your social security, Minimize your taxes.

How’s that for advice? Let’s try again.

Maximizing your social security = Minimizing your taxes.

That’s better. Strategy 1 helps you accomplish strategy 2. What if I told you, it’s possible to save nearly 400k in your retirement just by following this one piece of advice?

Let me illustrate with an example:

Assumptions

a) John and Melinda were born in 1961 and can claim social security beginning in 2023 at 62

b) They both had high paying careers and have estimated FRA benefits of $3,627

c) They need $100,000 of income through retirement to maintain their current lifestyle

d) They are debating between taking social security early at age 62 or waiting until age 70

Social Security

Looking at the chart below, the green bar represents the cumulative social security received if both John and Melinda delay their benefits until age 70. The red bar represents the cumulative social security received if they both claim social security at age 62. Our social security software uses a normal life expectancy of 85 for men and 90 for women.

As you can see, under a normal life expectancy scenario, choosing to delay would yield about $305,000 through retirement.

Taxes

Using tax software, we can estimate the amount of taxes that John and Melinda would pay in retirement, given different Social Security choices. Everything is in today’s dollars, we are just looking at federal taxes, and we are taking the standard deduction with no complicating factors.

Same assumptions as above, with a need of 100k income in retirement. 3 Scenarios as follows:

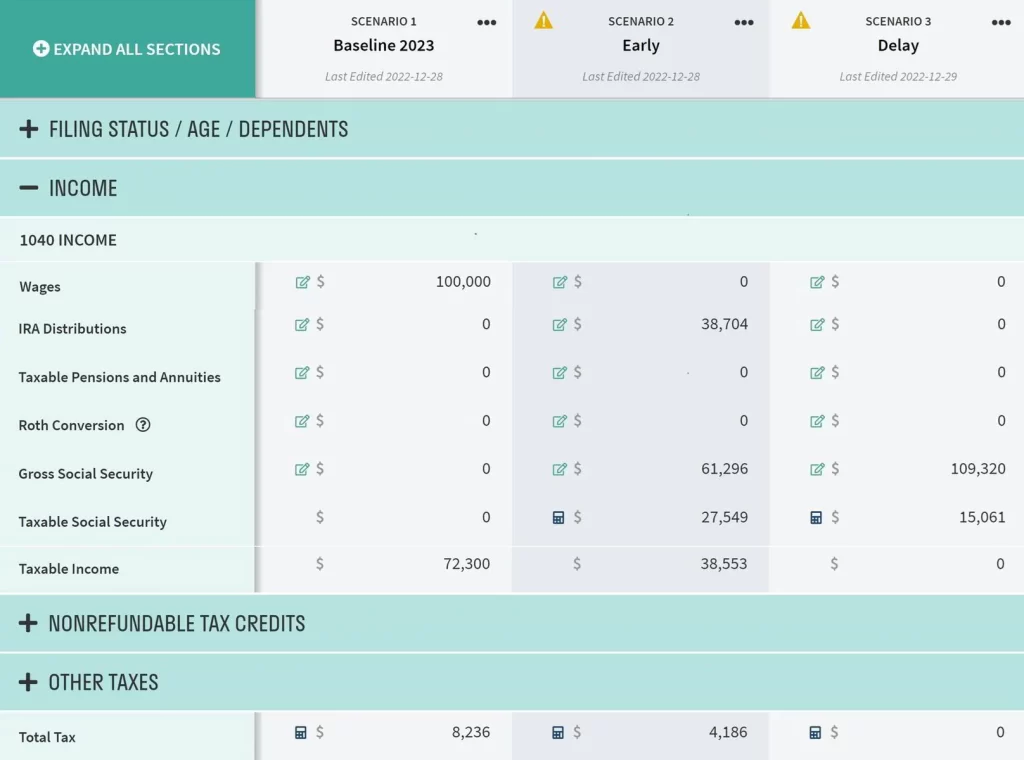

Scenario 1 – Baseline: This baseline scenario shows 100k of income from wages, prior to claiming any social security benefit. As you can see in the screenshot from our tax software, it would result in $8,236 in federal income taxes.

Scenario 2 – Claiming Early: If John and Melinda claimed early, they would have a total of $61,296 of social security income each year (today’s dollars). To get to the needed $100,000, they would need $38,704 of income from somewhere else. Most Americans have most of their retirement in qualified funds in 401(k)’s, Traditional IRA’s, etc. Assuming this was the case, John and Melinda would pay $4,186 in federal income taxes.

Scenario 3 – Delaying till 70: If John and Melinda were able to delay until age 70, they would have a total of $109,320 of social security income each year (today’s dollars). This would more than cover their required income. What’s even better, they would pay $0 in federal income taxes!! Imagine that… in Scenario 3, John and Melinda receive more income than both Scenarios 1 and 2, yet they pay no taxes!

See chart below:

Total Savings

Maximizing Social Security: $306,780

+

Minimizing Taxes: $83,720*

=

$390,500

*Assume 20 years of tax savings from age 70 to age 90

Conclusion

This is a simple example, and yes, it is true, most retirees will not have two spouses who can both max out the social security benefit and achieve almost 400k in savings. However, the principles remain the same even as the numbers change. Finally, keeping your taxable income as low as possible in retirement will generate more in savings than just what we’ve covered here, e.g. preventing higher Medicare premiums, avoiding the widow trap, and enabling you to do Roth Conversions.

Josh Bretl is a CPA who loves working with retirees. Josh teamed up with his father in 2003 at FSR Certified Public Accountants, Ltd. to build secure financial futures for retirees and pre-retirees in the greater Chicago area. He is proud to work at a family-owned firm that specializes in tax-focused retirement strategies.

Josh Bretl is a CPA who loves working with retirees. Josh teamed up with his father in 2003 at FSR Certified Public Accountants, Ltd. to build secure financial futures for retirees and pre-retirees in the greater Chicago area. He is proud to work at a family-owned firm that specializes in tax-focused retirement strategies.

0 Comments